Get Smart With Money (A NETFLIX Review)

The new Netflix documentary Get Smart With Money takes a look at regular people and how they can control their funds by killing debt, saving more, earning more, and retiring early.

I don't usually review movies but seeing as I have reviewed a couple of crypto-YouTube channels of late I thought I would try my hand at reviewing Get Smart With Money and seeing what happens. I did watch it after all and I suppose it is somehow related to the wonderful world of currency.

This won't be a traditional "movie review" as such but more of a lazy concept and methodology review mixed in with a little complaining and laughter. Kind of like if you were reviewing a food channel's recipe, you'd review the meal after eating it, but maybe also make remarks about the content like "this guy is a lunatic" Kind of like that.

Get Smart With Money: First Thoughts

If you haven't seen it, or not seen the trailer, look below.

Initially, my first thoughts from the first five or so minutes were "oh, here we go, we have an athlete, a couple of rich folks, and a talented blue-haired artist, gee, real people, c'mon".

I didn't think that these were regular folks that I could empathize with, but more so, people that had been specifically selected out of thousands of casting calls because of their looks and potential to succeed for the sake of the show as compared with regular salt of the Earth middle-class types that I could find something in common with.

I would have wanted to see younger folks or people just getting started in the big wide world of moolah because that is what the show focuses on in the beginning, the lack of financial education.

But then, rationality kicks in.

And like my big brother once said to me when I complained about a bad horror movie we were watching;

"If you want reality, look out the window dumba$$" ~ Andrei's big brother

Reality is mostly boring and slow-paced. A movie needs to be entertaining and a movie like this should also be informative. OK, I get it now.

A documentary film is at the end of the day part art, part fact, part fiction and probably, I don't know, thousands of hours of content that need to be sliced, diced, and edited into something nice to watch.

The show's participants eventually grew on me.

Get Smart With Money: An Overview

One of the striking things about the film format is that I wondered if it was a series. It's delivered like a show and when it gets to the end, you're left thinking another episode will start. But it doesn't.

I looked online and it seemed others were confused too. But nope, definitely a one-off movie and not a show or series of episodes. That was odd, but whatever.

The film looks at 4 sets of people that could maybe be described as middle-upper-class. They pair these 4 sets of folks up with financial guru types.

The Main Players

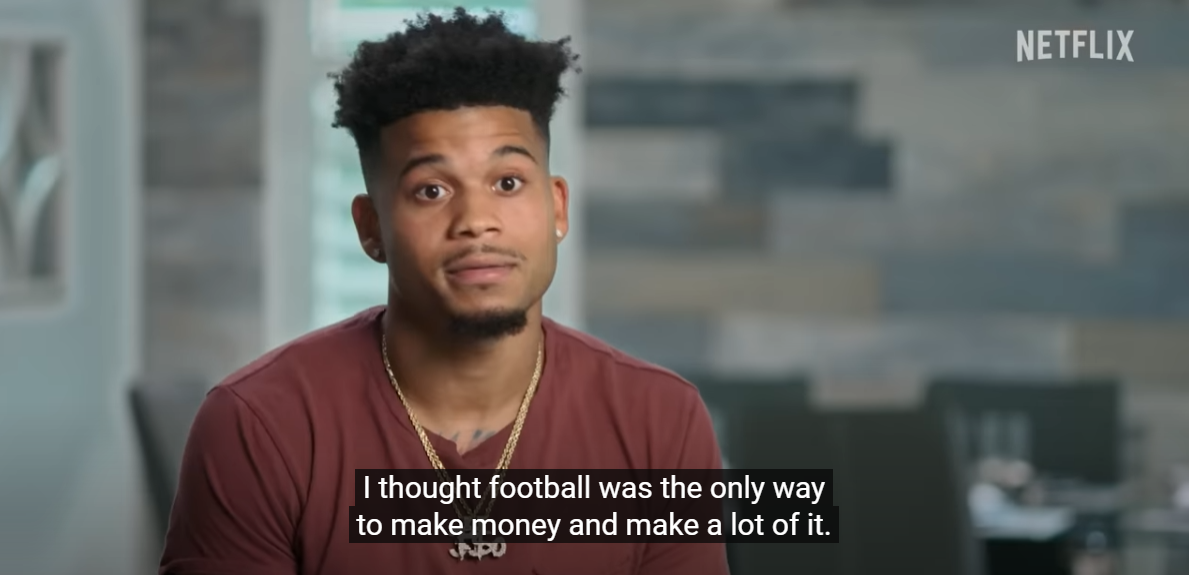

One of them, a guy called Teez plays professional football in the NFL for various teams in his snapshot of a career shown on screen and as you'd expect, he's obviously earning really good money.

Teez banked $1.6 million, for his initial contract and then was being paid 10k a week while on the practice squad. Eventually, Teez makes it to the main squad and is earning about 25k a week.

Teezs' issue is that if he's injured or dropped from the team, he makes no money, which is standard practice for most professional athletes. His other issue is that once his short-lived career is over, the money stops.

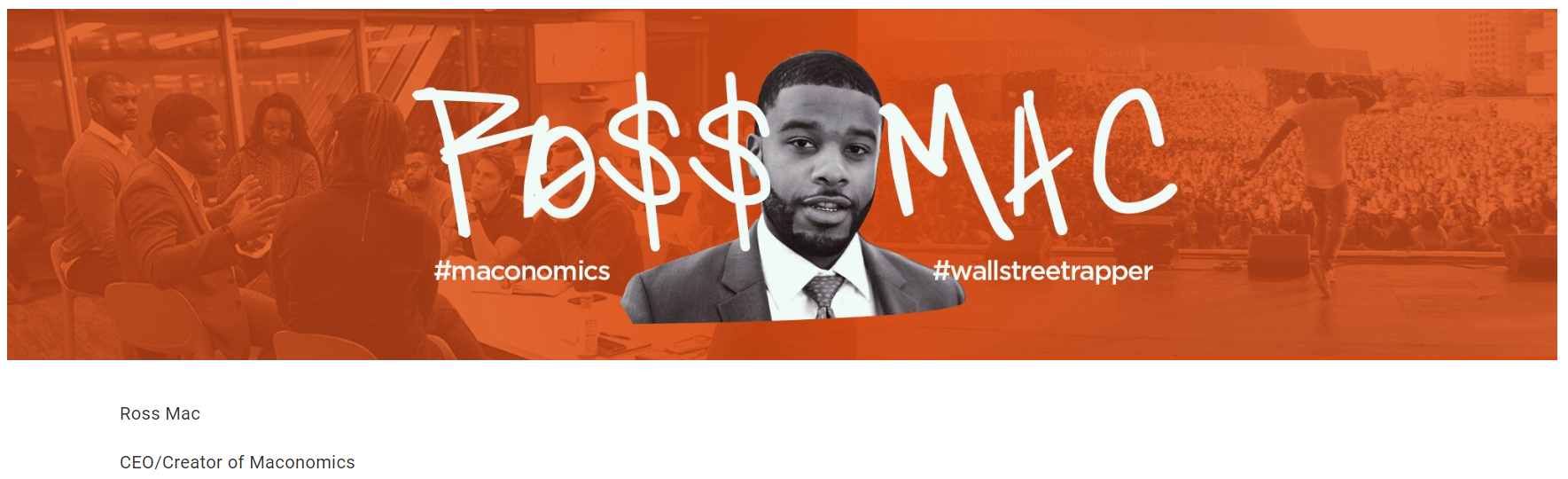

Teez is paired up with guru Ro$$ Mac.

John and Kim have a small family with two kids.

John is a stay-at-home dad that used to work as an engineer. His wife Kim is a psychotherapist and women's empowerment coach (whatever that means), she is earning $300k a year, and their issue is that as their money has grown, so have their bills and their spending.

John and Kim are paired with Mr. Money Mustache Pete Adeney.

The blue-haired artist is Lindsey. She seems to be that kind of cliche artist type. She's working two jobs as a waitress and server and is struggling with mental health issues and trying to figure out how to get her art off the ground and into something where she can earn money from it regularly.

Lindsey gets paired up with Paula Pant.

Ariana, we don't know too much about, or at least I don't remember or care enough to re-watch other than to say she seems to have an addiction to credit cards, and online shopping and has a bunch of student debt to pay off.

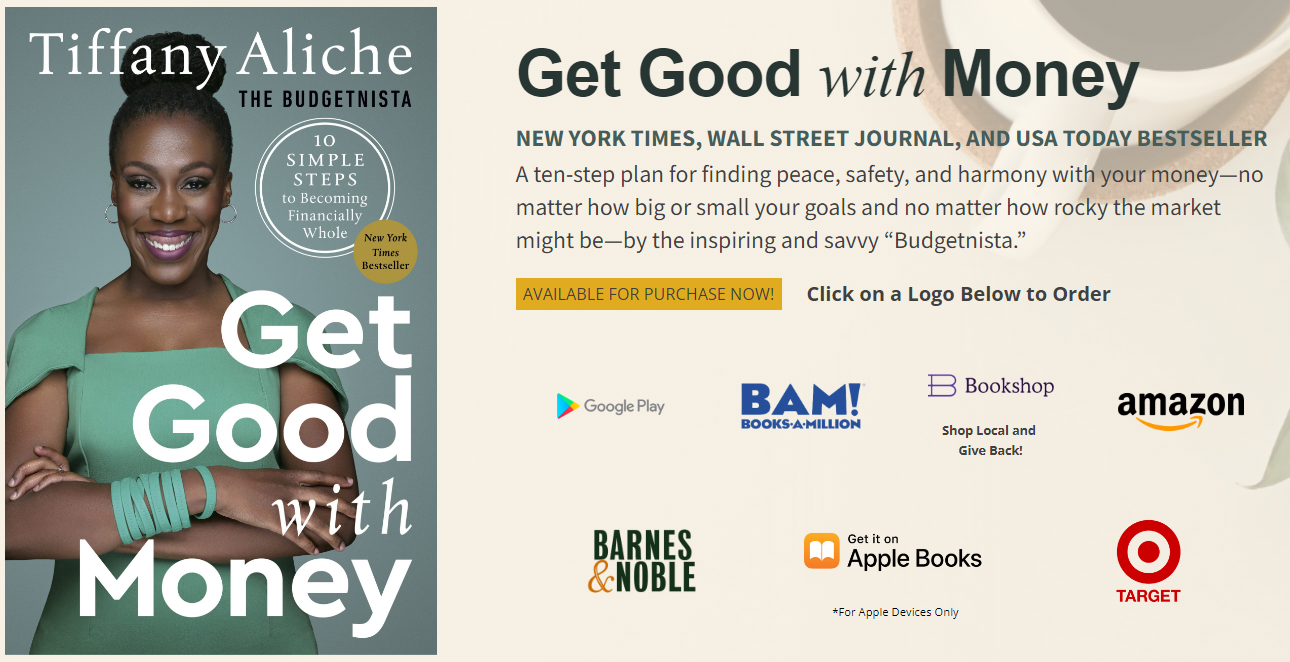

Ariana is paired up with Tiffany Aliche.

Big-Little Money Problems

Out of the 4, the artist chick Lindsey is the one that seems to be starting off from a lower rung on the cash ladder, and interestingly when the show finishes, without spoiling it too much, it appears she's still down there somewhere trying to figure it out.

This is where the cynic in me wonders how good the professional financial help and support really was from Paula Pant or if it was just a way for Paula to get herself out there a little more which is common among a lot of these finance and lifestyle coach types. You know write a blog, make some videos, eventually publish a book, and then do shows selling tickets and courses into eternity.

Then again, we are told Lindsey has mental health problems. So who's to say she wasn't given ample opportunities but for health or other reasons couldn't succeed?

I just would have wanted to see her do well (despite my personal disfavor of blue hair) because she seems to need it the most, while the other participants seem to be well educated, with good careers and good-paying jobs. In fact, this is the reason I only gave the film 3 stars and not 4 or 5.

If you're making a documentary film about how we all, as a society, need financial education, and how these modern-day finance wizards can help us change our financial futures, it's a bit sucky when 1/4 of the show's participants are not really that much better off in the end. And it's especially sucky when it's the one participant that needs the help the most. Come on bro.

The Finance Gurus: Who Are They?

Mr. Money Mustache

The participants are mentored by these modern-day Internet-era financial gurus that post inspirational videos on Instagram and have blogs, but honestly, I'd never heard of any of them except for Mr. Money Mustache, Pete Adeney.

MMM as he is known, is a finance blogger that says he is not a finance blogger and who seems to have worn the same shirt for the last decade (which I am sure he is proud of), practicing what he preaches I guess you could call that. I like Mr. Money Mustache and have read his stuff off and on for some time.

I don't necessarily agree with everything he says, obviously. MMM is mostly all about living frugally and investing the savings, saying things like "ride wherever you can" which not only isn't practical when you have kids but also, hey man, I only got one life to live, I'd rather save an hour-long trip to work and back on my bike and turn it into 15 minutes in my car! Time is the most valuable thing in the Universe!

I also think it's weird that MMM recommends and promotes Credit Cards on his blog (likely an affiliate-type deal where he is paid for the referrals). I'm sure he'd say this is good for emergencies or travel, but still, seems a bit weird, not hating on the guy, just saying.

The show focused heavily on getting rid of Credit Card debt. But whatever. I have a resources page too. Just mine doesn't have credit cards on there.

Out of all the gurus, MMM is my favorite.

Bonus bit of info: I once interviewed a guy called Mr. ERB (Early Retirement Bitcoin). This character was inspired by MMM to begin living frugally and saving everything else and investing it. The spin he put on it though was that he decided to invest in Bitcoin and only Bitcoin. Read about it here.

Paula Pant

Paula operates a blog and podcast called Afford Anything and it seems she's the female version of MMM. Paula is a big advocate of the Financial Independence, Retire Early (FIRE) movement.

Paula, like MMM, makes money through affiliate sales on her website, real estate courses, public speaking, and book sales.

Ro$$ Mac

I'm not too sure what this guy does. His website domain is rossmacmusic.com which makes you think that he might be some kind of musician, he calls himself the #wallstreetrapper.

I'm too lazy to dig deeper so I'll just copy-paste a quote from his bio;

Ross Mac is an Ivy-league (Wharton School of Business) educated, Chicago native dedicated to increasing access to financial education and literacy. As a former Wall Street professional for Morgan Stanley and Grosvenor Capital, Ross is now a media personality for BET, Revolt TV, and The Street who uses his brand to empower people through merging education and entertainment. He’s the creator of the Maconomics digital series where he gives plain advice to people who may not have access to the traditional avenues to receive this information.

Tiffany Aliche

This lady calls herself "The Budgetnista". Tiffany is a best-selling author and speaker. Her book Get Good with Money was a New York Times and Wall Street Journal bestseller and is rated 4.9 out of 5 stars on Amazon.

Mr. Money seems to be the more senior finance and lifestyle wizard of the lot and his advice is echoed by all of the other gurus. This becomes apparent really quickly. The idea is this:

- Save money.

- Pay off debt.

- Invest the rest.

Solid advice. Do it.

Negative Reviews of Get Smart With Money

I looked online and read comments and reviews from a bunch of people that had seen the film and were of course complaining about it because I don't know, I guess sitting on their couch, watching the movie didn't put money into their bank account.

It's funny how so many of these same types of people, no matter what topic, niche, or aspect of life, when you tell them; stick to the basics, and get the fundamentals right, they begin to say things like "oh I was expecting more" or "it was very general advice, I knew that already".

Whether it's calories-in, calories-out, or save and invest, what they don't get is that these basics, these fundamentals, are just that, the basics, you need to get these things right and of course, most never do but yet they want to complain about their situation.

As a crypto blogger, I get people that read these posts of mine, which interestingly enough, as you would have noticed are not even really about making money, but occasionally I will have people ask me which crypto to invest in or when they should sell. I don't involve myself in that and never will.

Stick to the basics. The rest is just entertainment and education.

The reality is that most people are kicking along paycheck to paycheck, up to their neck in debt, and I don't want to be the one to be blamed for ruining their life, which is why I don't like to get into that stuff, but also, I like to leave the price predictions to people like this guy because guess what, they almost always get it wrong, and it's pretty funny to watch from the sidelines (schadenfreude? Maybe.).

Personal Experience Time

I've always been OK with money, meaning that while I wouldn't call myself frugal, I've just never been a big spender. I don't buy flashy cars, I rarely even buy new clothes, but when I was young, dumb, and full of ***, I fell into the credit card scam and debt trap too, I got a credit card because I was going overseas to meet (chase) my now "life partner", it was supposed to be an emergency card and 4 or 5 grand worth of "emergencies" later I was wondering what the hell happened. '

But mostly when I look back now, I was lucky that I had immigrant parents from the Eastern block of Europe who told me "debt is bad" and "credit cards are evil". So I already knew what I was doing was stupid and had some leverage going forward.

My better half eventually took my credit card and other personal debts and put me on the fast track to paying them off. It's amazing how much money is left over at the end of the day when you no longer have to pay back other people's money that you "borrowed", it's almost like you could have saved that money in the beginning and wouldn't need to borrow it in the first place!

Now you know why I hate credit cards.

But saving money and paying off debt while good, isn't going to get you rich or retired.

How to Retire Early

The film's focus is mostly on the points laid out above. They all sing from the same hymn book on this topic because it works. Save money, pay off debt, and invest.

Methods

At one point in the film, guru Paula that is assigned to help our blue-haired artist friend Lindsey and tells her to "look into" NFTs. I was a bit stunned she didn't take the opportunity to show her the process of minting an NFT.

You can't just tell someone, "hey, look into NFTs" and expect it'll make any sense. NFTs are a different language to someone that has used a paintbrush and sewing machine throughout their art career. This was a missed opportunity in my view.

Take the horse to the water, if he drinks, he drinks, but take him to the water, don't just tell him about the water and expect it to happen.

This NFT comment was one of the most unique methods mentioned in the film, the rest were standard practice.

Let's take a look at some of the other more practical methods talked about;

- Pay off bad debt.

Credit cards, personal finance, and car finance are the big ones, hit these first.

Homes and mortgage payments don't necessarily fall into this category because they can be considered assets at some point in time. Student loans also need to be paid off but not as urgently because the interest is much lower. So when paying debt off focus your methods on those high-interest killers. And when doing so, create separate bank accounts and ask your employer to pay into those.

Set up emergency fund accounts so that you don't need to rely on credit cards. - Be frugal, save money.

Don't spend money on flashy cars, cut your own hair (come on ladies, you can do it too!), shop at bulk buy type places like Costco, and don't buy stuff you don't need. But don't let it get in the way of living a good life. Holidays/vacations, time with kids, having fun, and creating memorable life experiences are great things to spend money on.

Set up emergency holiday/dream accounts so that you can save for these things. - Earn more.

If you can do it at work, go for it, climb that ladder! Otherwise, set up a side hustle and try to scale the side hustle to the point where it begins to become your full-time hustle if you can. - Invest.

Whatever you can save, invest, if you earn more, invest, if you have something left over, invest. The show doesn't spend too much time getting into specifics. other than saying that you should invest in index funds like the S&P 500, and NASDAQ 100, as well as stocks and real estate. At one point they talk about using things like E-Trade to regularly make your investments.

They also touch on real estate saying that if you can scale down and buy other properties you should.

How Much Money Do you Need to Retire?

The film explores the topic of how much money is needed to retire comfortably, they call this the FIRE number (remember, Financial Independence, Retire Early), they say that this number is 25 times your current living expenses.

For most people, this works out to be between $1.0 - $2.0 million dollars. Of course, this depends on many factors. How old you are, whether or not you have kids, where in the world you live, and so on.

The FIRE idea culminates as follows.

Once you have your 1 or 2 million big ones invested into stocks and maybe also real estate, even if there are no gains in prices or value and no dividend payouts, it will still be enough for you to be able to draw down from monthly or quarterly, as you need to, in order to live your life without having to work.

For example, if you want to be comfy, like really comfy, let's assume $80k is your FIRE number, you need $2 million, which means you can withdraw 4% per year for 25 years. So it all really depends on how long you plan on living...or living while retired without the markets killing your investments.

Conclusion

All in all a pretty good film. Don't listen to the naysayers and that includes me. The general message is a good one. Save money. Pay off debt. Invest the rest.

Thanks for reading and cheers to our collective early retirement.

Want to Keep Reading?

- Blockchain Backer - A Crypto YouTuber Review (Read THIS Before Watching)

- How Does OpenSea Make Money? (This Will SURPRISE You)

- NFT Companies | The Most Ultimate List Ever

- GameStop NFT Marketplace Review

Want to know how you can support Crypto Fireside?

Sign up below. It's free, it's easy, and it allows you to comment and join the discussion 🔥