The Dollar Dilemma: Why Not Every Dollar Is The Same?

Have you ever thought about the idea that not all dollars are created equal? On the surface, it may seem like a really odd concept.

Have you ever thought about the idea that not all dollars are created equal? On the surface, it may seem like a really odd concept. After all, isn't a dollar always worth a dollar?! The answer, surprisingly, is much more complex than it appears.

There are different characteristics, but also risk profiles associated with different types of dollars, and it's essential to understand the nuances when holding dollars in your portfolio. Let's delve into this surprisingly interesting topic by examining several different types of dollars: traditional U.S. dollar in a bank (small and large), U.S. dollar in cash, and stablecoins like Tether’s USDT, Maker’s DAI, and Liquity Protocol's LUSD which are all USD-pegged stablecoins.

Seemingly all these forms of a dollar possess are equal to one U.S. dollar, but they hold different practical implications that give them unique forms of “value.”

We will go through these dollar differences and illustrate how their unique characteristics influence their roles in our financial systems and digital economy. Whether you're an anon crypto enthusiast, a seasoned financial analyst, or just curious about the subtleties of money, this exploration will give you new insights on the different dollars.

A dollar in a bank

When you deposit a U.S. dollar into a bank, it doesn't just sit there idly. It gets swept up into the broader financial system where it works hard for the bank. Your deposited money is used by the bank to offer loans to other customers and earn interest, creating a cycle of financial activity. They are allowed to do that, because of the so-called Fractional Reserve Banking. Until the beginning of 2020 banks in the US had a reserve requirement of 10% (i.e., 0.1), meaning banks could lend out 10 times more than their reserves.

In March 2020, the Federal Reserve set the reserve requirement for U.S. banks at … 0%. The change was made to support lending and liquidity during the COVID-19 pandemic. This means that, contrary to previous practices, banks are not required to hold any specific percentage of their deposits as reserves.

This is exactly the reason why banks don’t have enough cash reserves on hand to cover all of their deposits. This is also the reason why bank runs are possible and happen each year.

Value of a bank dollar

The value of the bank dollar depends on several factors. Primarily, its value is linked to the stability and trust in the specific bank you have your funds at. In addition, the value depends on the whole U.S. banking system and the U.S. government.

Bank deposits are FDIC insured up to $250,000, providing an additional layer of protection. In this regard, your first 250k dollars in a bank have another risk profile than the dollars you hold in excess at such a bank.

The risk profiles of a dollar in a small bank versus a large bank differ, too. While both types of banks are usually insured, smaller banks might offer higher interest rates to attract depositors. However, these institutions may also carry a higher risk of insolvency. The dollar in a small local US bank is less safe as it might not be bailed out by the government while the too-big-to-fail banks usually are saved by the government when needed. Thus, we have recently seen people moving their cash (that is not insured by the FDIC) from smaller to larger banks.

Liquidity-wise, when converting dollars into other currencies, this is generally a non-issue at larger banks and exchange offices due to their volume of business but may be a factor at smaller, less frequently used outlets.

Large banks, on the other hand, might offer more stability, but their interest rates could be less competitive. Furthermore, having your money in a large bank doesn’t mean your funds are completely safe. Only in 2023, we have examples such as with Silicon Valley Bank (SVB) which failed when a bank run was triggered after it sold its Treasury bond portfolio at a significant loss, causing depositor concerns about the bank's liquidity.

A dollar in cash

Compare this with a cash US dollar bill. The US dollar bill is a bearer instrument, which means that whoever holds it owns it. This form of the dollar is immediate and tangible — you can use it anywhere, anytime, without the need for an intermediary. But it comes with its own challenges. Physical cash can be lost or stolen, or even damaged to the point of being unusable. It's not practical for digital or large-scale transactions, and it doesn't earn interest.

The US dollar is one of the most liquid assets on the planet. As the world's primary reserve currency, it is accepted almost everywhere and can be readily exchanged for other currencies at places like banks and currency exchange offices.

Holding cash doesn't require a service fee or maintenance charge, unlike some bank accounts or other financial services. However, the 'cost' can come in the form of foregone interest that could have been earned if the money were invested. Indeed, since cash is not invested, it depreciates at the pace of inflation. Additionally, securely storing large amounts of cash may require purchasing a safe or renting a safe deposit box, which adds to the cost.

Cash transactions, unlike transactions enabled by dollars in the bank or centralized stablecoins, are trustless and non-censorable: there is no way of restricting cash to specific use cases or enforcing limits (unlike with CBDCs).

Cash transactions provide a high degree of privacy, as they do not inherently generate a record or leave a digital trail like electronic, card-based transactions and stablecoins. However, it's worth noting that in the U.S., certain large cash transactions are subject to being reported to the government to prevent money laundering or other illicit activities.

Moving large amounts of cash across international borders is also a complex and often legally sensitive issue in many countries. This activity is heavily regulated due to concerns about money laundering, terrorism financing, tax evasion, and other illegal activities. Most countries have established specific laws and reporting requirements for transporting significant sums of money. For instance, it's commonly required to declare cash amounts exceeding a certain threshold (e.g. $10 000) at customs.

Even though there is a widespread misconception that crypto is often used for illicit transactions, data shows that cash actually is and always has been the form of money most preferred by criminals.

Another potential issue with cash is that assessing whether a dollar bill is real or counterfeit can be challenging for an untrained eye. Devices like counterfeit detector pens or UV lights can help detect fake bills, but you can’t expect that everyone would start looking at every banknote with a special device to see whether it's authentic.

A USDT Dollar

As we transition into cryptocurrency, let's look at USDT, a stablecoin that claims to be backed one-to-one by U.S. dollars in reserve. Its centralized and opaque reserve management has invited controversy and a higher risk profile. The value stability of USDT depends on the trust that Tether, the company behind USDT, actually holds the promised dollar reserves.

Over the years, there have been significant doubts and reports that Tether does not have the 1:1 collateral it claims to have. In 2021 the company was fined over $18 million by a US judge, and in 2022 Tether was fined another $42 million, both times for deceptive information about their collateral. The court found that Tether was only backed 26% between 2016 and 2018.

Tether has been promising a full audit by an external auditor for years, which is yet to happen.

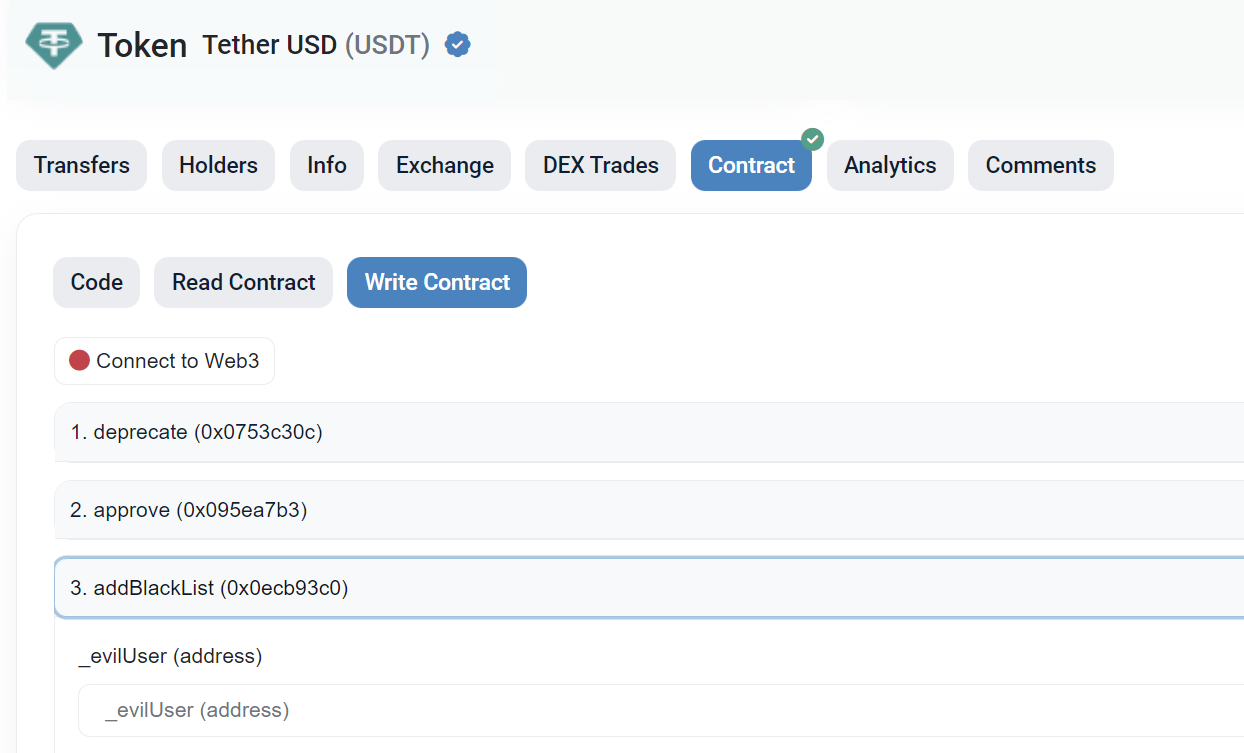

Furthermore, the biggest stablecoin by market cap USDT has a function (_evilUser) in its smart contract which can freeze funds in a user’s self-custodial wallet.

In other words, you are far from having complete control of your dollar. At the time of writing, there is nearly 100 billion USDT, which is equal to roughly 70% of the whole stablecoin market supply.

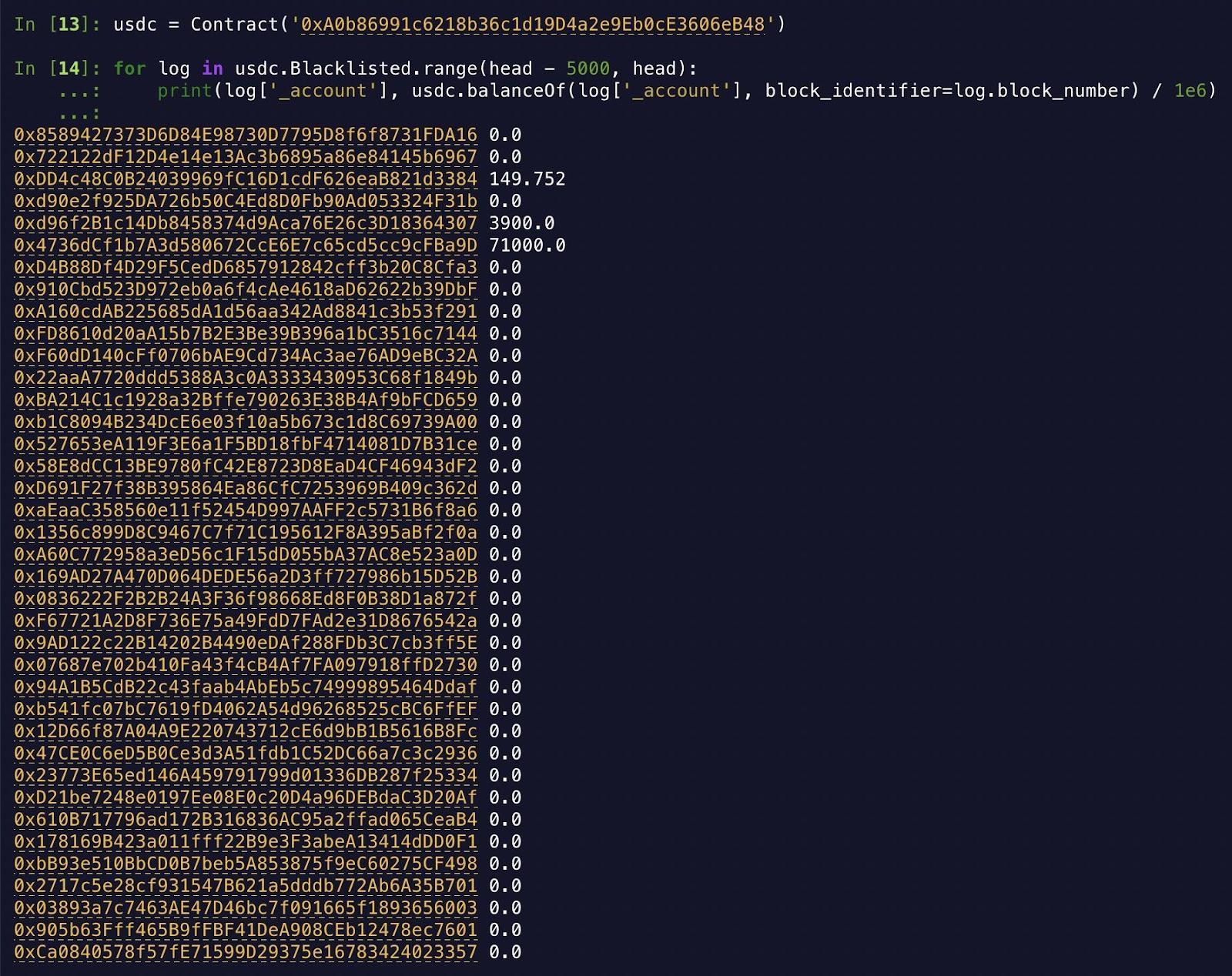

USDC also has the same censoring function. They have used it in situations like the one with the Tornado Cash which was sanctioned by OFAC. Circle, the issuer of USD Coin (USDC) stablecoin, froze over 75,000 USDC worth of funds linked to the 44 Tornado Cash addresses sanctioned by the U.S. Treasury’s Office of Foreign Assets Control (OFAC).

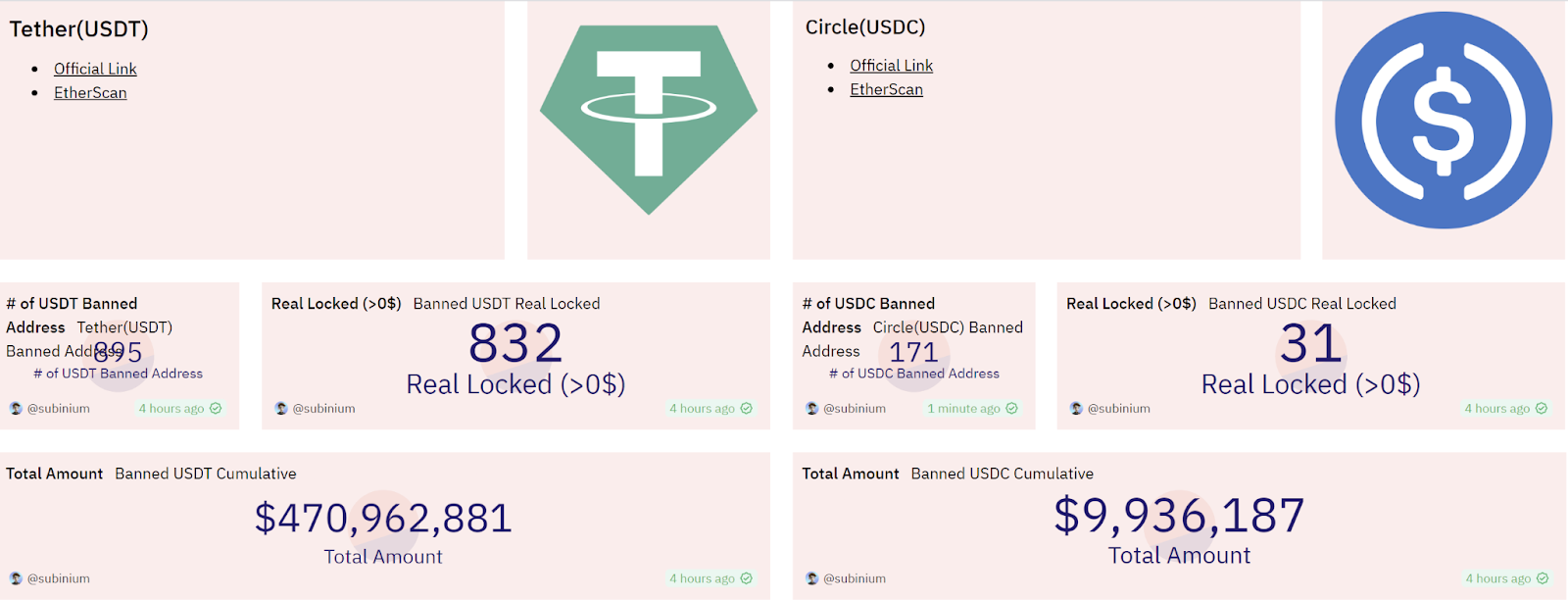

In total, Tether and Circle have banned over 1000 user addresses possessing close to $500 million.

A DAI dollar

DAI, a stablecoin created by the MakerDAO protocol, offers a contrast to USDT. It's decentralized by design and collateralized by various assets, including mainly Real-World Assets (RWA), but also ETH, staked ETH, centralized stablecoins, ERC-20 LP positions, and others. Maker has also moved $500 mil of DAI’s collateral into Coinbase’s centralized custody. All this mixed collateral increases significantly the risk behind Maker.

In contrast to USDT and USDC, DAI has no built-in freeze and blacklist functions. Nevertheless, as mentioned above, DAI uses some centralized stablecoins like USDC as collateral. Circle can also freeze such USDC backing.

The RWA collateral on the other hand bears the risk that you cannot check on chain in real time what is its actual value and it's also nowhere near as liquid as most onchain assets.

On the positive side, there are billions of DAI on the blockchain, which makes it highly liquid. You can move your DAI 24/7 on chain, plus there are multiple centralized and decentralized exchanges and other solutions that you can use for off-ramping your Maker stablecoin.

A LUSD dollar

Finally, let's look into Liquity's LUSD. A decentralized stablecoin, overcollateralized by Ethereum. So here, you don’t face the fractional banking issue that banks have. As a stablecoin, here you also have access to your dollar 24/7 and can move it in a matter of seconds to different wallet addresses, off-ramp it, or pay directly with LUSD using something like the Holyheld or Wirex cards.

Liquity operates with an immutable contract, making LUSD almost as resilient and unstoppable as the Ethereum network itself. This means that LUSD is not subject to many of the same risks as centralized stablecoins. Liquity’s smart contracts have been live for more than two years. The immutability, given the length of time Liquity has been around, really puts it among the best in class with respect to risk.

A further proof is DeFi Safety’s ranking which gives Liquity a 96% score and one of the top spots among 260+ DeFi protocols. DeFi Safety’s protocol reviews are: “A quality assessments that scrutinize major key elements of deployed DeFi products to produce an overarching safety rating that indicates the quality of development processes and accompanying documentation.”

Unlike traditional dollars, LUSD truly belongs to the holder. No central authority can freeze or seize LUSD funds, which represents a paradigm shift in the concept of monetary ownership.

LUSD is also directly redeemable to ETH and cannot be minted out of thin air. For every LUSD in the market, there is X worth of Ether backing it. LUSD's unique model eliminates the need for trusted third-party collateral. You can always see the backing of LUSD through real-time auditing with Etherscan or Dune Dashboard here.

So with LUSD, you have probably the most decentralized, transparent, trustless, and censorship-resistant dollar there is. LUSD is not the ultimate stablecoin, its peg is not always perfect and LUSD is much less scalable compared with centralized stablecoins, but if you’re aiming for decentralization and security, look no further.

Conclusion

Not all dollars are created equal. Each form carries unique risks and advantages, shaped by factors like control, access, stability, interest rates, censorship resistance, counterparty risk, etc. These profiles are shaped by various factors, including trust in institutions, market volatility, algorithmic control, smart contract risks, and overall economic resilience. There is always a trade-off in stablecoin designs.

As the financial landscape continues to evolve, understanding these nuances becomes increasingly vital. Whether it's a traditional bank-held dollar or a decentralized stablecoin, the value of a dollar extends beyond its face value — it's also defined by the systems that create, manage, and circulate it.

The goal of this article is not to make you convert all your dollars into one type but to deep dive into the different characteristics and risk factors some of the popular traditional and blockchain dollars possess. No matter whether you are an individual, institution, or DAO with a significant treasury you should always diversify your dollar holdings based on your needs and risk appetite.