Can You Invest in Crypto Tax-Free?

🔥Crypto Fireside #34— Interviews with crypto people.

🔥Crypto Fireside #34— Interviews with crypto people.

🔥Hello! Who are you, and what do you do?

PC: My name is Palmer Czaplicki. I’m an investor first and a facilitator of legal structures second. I first got involved with Cryptocurrency in early 2017 and have been hooked since day one. Starting in October of 2020, I have facilitated a legal process called Qualified Rollover that gives investors more freedom to invest freely. I do this through my company Lion’s Share Wealth.

“Over and over again, courts have said there is nothing sinister in so arranging one’s affairs as to keep taxes as low as possible.” -Court Ruling by Circuit Judge Learned Hand, 1947

Conventional wisdom says to contribute to qualified retirement plans (401[k], IRA, 403[b], 457[b]) and, in return, save some taxable income now for a small deduction. Sounds great in theory, but you’re unknowingly setting yourself up for financial ruin later in life (more on this later). While there are various types of qualified plans, I will focus on 401(k) for simplicity.

If you live in the USA, there’s a good chance you or someone you know has one, as there are more than 50 million Americans with shy of $6 Trillion in their 401(k) plans. 401(k)’s have downsides, including lack of asset class options (typically restricted to Mutual Funds), Contribution Limits ($20,500 per year in 2022), Prohibited Transactions, Growth is Subject to Volatility of the Market (the Dow Jones has a 43% drop every 9.8 years on average), and worst of all Performance Drag. Forbes estimates that Advisory Fees and Transaction Fees can cost you up to 6.22% per year, severely eating away at your gains.

I focus on re-characterizing those qualified retirement plans so you’re in complete control of your investments. With a Qualified Rollover, you can invest without restriction in Marketable Securities (Stocks), Alternative Investments (Crypto, Precious Metals), Real Estate, and more. You can choose where you allocate your fund and can move freely from one asset to another to follow market cycles. Most importantly, every Qualified Rollover requires a letter of approval from the IRS to move forward with this process.

🔥What’s your backstory, and how did Lion’s Share Wealth come about?

PC: In 2011 I started working for a multi-national financial services conglomerate as a business developer that provided extended service contracts on consumer electronics. While I didn’t delve into the actuary & underwriting side of the business, I had a basic grasp of how insurance works. This knowledge has translated into the world of Insurance Contracts, which follow many of the same principles. In mid-2020, I discovered how people can self-direct their 401(k) to crypto, and in October 2020, I started providing this service.

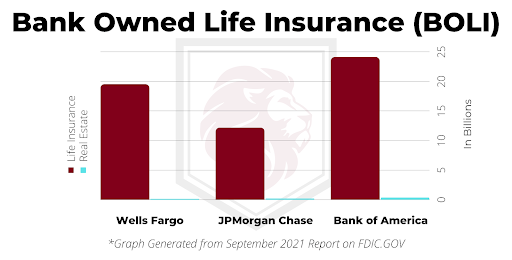

A cornerstone of the Qualified Rollover strategy is Life Insurance Contracts. I will be the first person to admit that Life Insurance is probably one of the least exciting topics in the world. However, the fact is, Life Insurance is the #1 safest asset class in the world by a long shot. Let’s look at a graph to show how much Life Insurance the biggest banks in the country own (BOLI = Bank Owned Life Insurance) vs. their #2 largest asset, Real Estate (mortgages), represented by the blue bars.

Why do banks own tens of billions of dollars worth of life insurance? The answer is relatively simple:

- It’s safe.

- The distribution (death benefit) is tax-free.

- They’re guaranteed to get it.

- Protected Principal (growth not subject to the volatility of the market).

It may come as a surprise that a Life Insurance Contract is one of the safest assets in the world. Unlike a house or a car, you can’t lose an Insurance Contract in a flood or fire. Unlike cash or jewelry, someone can’t steal your Insurance Contract. As a real-world example, if you have an Insurance Contract, you can use the Cash Value as collateral for a loan at a lower rate than a house or car. In the eyes of a bank and being a low risk, if you were to default on the loan, the lender can attach to the death benefit, which they’re 100% guaranteed to receive.

Would you rather do what everyone else is doing, or would you instead do what the big banks are doing?

Typical life insurance you get from an agent should be called death insurance because that’s when the benefits usually kick in. However, there are ways to use Insurance Contracts while living to secure your financial future, including enjoying a predictable tax-free retirement, paying for long-term care while you’re alive, getting out of personal debt, starting a business, estate planning, creating a college fund, and more.

Bottom line: Life Insurance is what the ultra-wealthy have used for centuries to create generational wealth and grow their financial future.

🔥Describe the process of launching Lion’s Share Wealth.

PC: I wish I could say the launch of Lion’s Share Wealth was exciting as the launch of a new Crypto/Blockchain project. Unlike the people you’ve previously interviewed who spend countless hours launching their projects to perfection, launching Lion’s Share Wealth wasn’t nearly as groundbreaking. There wasn’t a 9-page whitepaper, an ICO, pre-sale, or a development stage. After operating under a law firm’s umbrella for several months, I started my agency to spread the word. All that changed in my day-to-day operations was introducing myself as the Founder of Lion’s Share Wealth instead of representing a law firm.

Since launching Lion’s Share Wealth, I’ve worked tirelessly to promote Qualified Rollovers and surround myself with movers and shakers across many sectors. My ultimate goal is to create an ecosystem for all things relating to wealth creation and wealth preservation. I’ve surrounded myself with experts in their respective fields, including Crypto, Real Estate, Stocks, Private Lending, and Joint Ventures. I refer to outside experts for wealth creation, and I facilitate tax-advantaged programs to work in unison regardless of the asset class. I constantly forge new strategic ecosystem mergers with like-minded individuals such as tax professionals, RIA’s (Registered Investment Advisors), and Wealth Managers. Instead of being competitive, I prefer to work together to provide better services to investors.

🔥Why did you choose Qualified Rollovers why not some other product or service for wealth creation and preservation?

PC: Based on every conversation I’ve ever had, 99% of people don’t know the terms of a 401(k).

As a case study, I challenge you to read the tax code Section 401, subsection K, to see if you can make any sense. It’s a multi-thousand-word monster, and you’ll realize you can’t understand the first paragraph. Even though it’s indecipherable unless you’re the one who wrote the code, it’s a household name. When the government created the 401(k) in 1978, it wasn’t originally supposed to be an Employer-Sponsored Program.

At the time, employers contributed to their employees’ Pension Plans, which was extremely risky for the employer. In 1980 a savvy financial consultant established 401(k) programs where the employee would contribute their salary, and the employer would match (Defined Contribution). Contrast this to Pensions which the employer signed up to write a blank check to pay the employee as long as they live (Defined Benefit). In the interest of not writing an in-depth thesis, know this: when an employer sponsors a 401(k) instead of a Pension, the employer wins, and the employee loses. For reference, Congress members have a Defined Benefit (Pension) program called FERS (Federal Employees Retirement System).

Today, 401(k) holders face four huge drawbacks:

- Lack of asset class options (typically limited to Mutual Funds)

- Performance Drag (expenses and advisor fees) can cost up to 6.22% per year

- Growth is subject to the performance of the market (43% drop every 9.8 years on average since 1896)

- Contribution Limits (as of 2022, you’re limited to $20,500 per year)

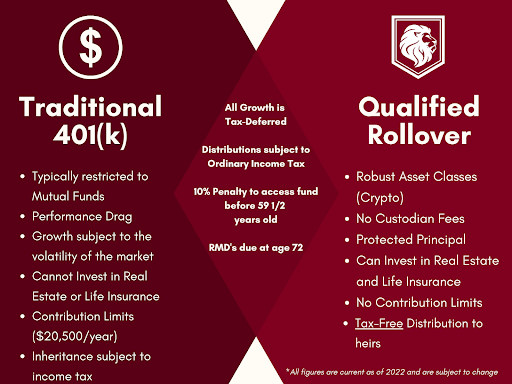

There’s a better way to manage your fund with a Qualified Rollover

Let’s look at the similarities, and differences, between a traditional 401(k) and a Qualified Rollover with a Venn Diagram:

As you can see, they share some similarities, and there are areas where the Qualified Rollover shines above a 401(k). A Qualified Rollover puts your Qualified Money in your control to invest in more robust asset classes and pass on a tax-free legacy to your heirs.

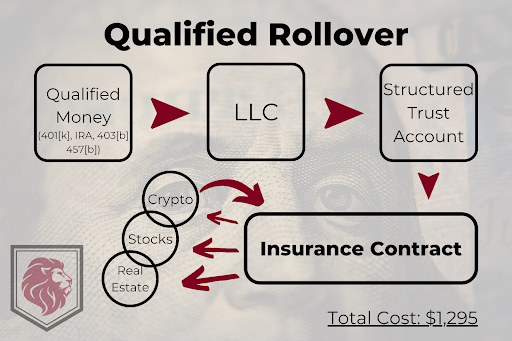

I facilitate the legal structures for a like-kind transfer of your Qualified Money into your fund, similar to a Family Office. After approximately 60 days of legal work, you have full access to your fund to invest in Crypto on a tax-deferred basis. You’re now wholly controlling your financial destiny and no longer subject to market volatility or advisor fees. The total legal cost for a Qualified Rollover is $1,295 regardless of the Rollover amount.

Here’s a flow chart of the Qualified Rollover process:

Life Insurance Contracts are a cornerstone of this strategy as it allows you to pass on your wealth to your heirs tax-free. You delegate precisely how the death benefit is treated upon your passing. Let’s say you don’t have a person you want to receive the tax-free death benefit; you can choose Charities that will receive the benefit, for example.

🔥How are you doing today, and what does the future look like? Let’s talk numbers!

PC: Let’s do a comprehensive breakdown of the numbers when a person wants to explore a Qualified Rollover.

When I speak with someone who wants to explore this option, I always start with the insurance first to ensure you’re medically approved. I must collect a bit of personal information, which I take to a Mutual Insurance Carrier, and they produce a breakdown document called an Insurance Illustration.

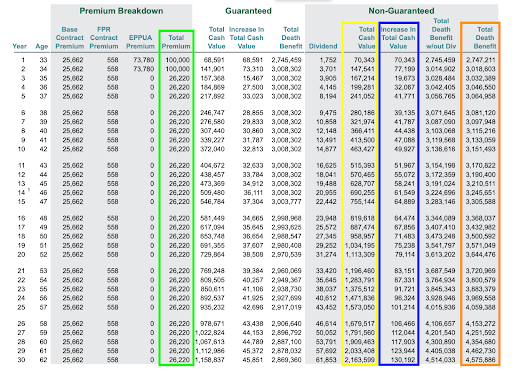

An Insurance Illustration serves to show precisely how your Insurance Contract will perform from Day One until you’re 120 years old. For illustration purposes, let’s say you have $200,000 in your 401(k) that you wish to Rollover. In tune with sticking to IRS rules, the $200,000 must be split into a minimum of two equal contributions of $100,000 each.

At the top of this chart, you see three distinct columns. From left to right:

Premium Breakdown

- “Premium” is an Insurance term meaning contribution. In this illustration, you’re contributing $100,000 in year one and $100,000 in year two. “Base Contract Premium” and “FPR Contract Premium” are the bare Cost of Insurance for the Death Benefit. “EPPUA” is Paid-Up Additions which is Over Stuffing a Life Insurance Contract with Cash Value.

- You may wonder what Paid-Up Additions are. In the interest of not deviating, the IRS has rules on how much Premium you can contribute to a Life Insurance Contract with how much death benefit there is. There’s a point where you cannot contribute more Premium without increasing the Death Benefit called the MEC Limit (Modified Endowment Contract). In this Illustration, I have avoided the MEC Limit.

Guaranteed

- Whole Life Insurance Contracts have a contractual Guaranteed Rate of Return not subject to market fluctuations. Whether we’re in a raging bull market or a falling bear market, you’re constantly earning the same rate of return.

Non-Guaranteed

- All Mutual Insurance Carriers provide Non-Guaranteed Dividends, a bonus provided by the Insurance Carrier. As the name would suggest, these Dividends are Non-Guaranteed. Even though they’re non-guaranteed, Mutual Insurance Carriers have paid them every year for centuries. I primarily work with an insurance carrier in business for over 170 years (I cannot provide their name in this article), and they’ve paid their Non-Guaranteed Dividends every year since they formed. Think about it this way; they’ve paid these dividends through the American Civil War, WWI, The Great Depression, WWII, the Dot-com bubble, and the Financial crisis of 2007–2008. While I cannot guarantee insurance carriers will pay these every year in the future, the chances are pretty good.

I will be referring to all growth of Guaranteed and Non-Guaranteed combined. Together, these have a gain of about 5% per year.

Special Note: You earn this Internal Rate of Return in addition to the gains you make in Crypto.

Now let’s break down the smaller columns, which I’ve overlaid different color boxes.

GREEN: The total Premium contributed each year. After the initial $200,000 is spread over two years, the cost of insurance is to continue the rise of the death benefit is $26,220 per year which can be paid with your Crypto gains, withdrawn within 30 days, and placed back into Crypto.

YELLOW: The total cash value you have access to in any given year, which you can utilize to invest in Crypto.

BLUE: The total increase in cash value each year of your Internal Rate of Return.

ORANGE: The total amount of death benefit that will be passed on to your heirs tax-free (less the taxes owed upon death). On day one after contributing $100,000, there’s a death benefit of $2.74 Million which grows to $4.57 Million at age 62.

Note: One of the beautiful things about Life Insurance is that you can access a portion of this Death Benefit while you’re alive to pay for living expenses should you require care later in life.

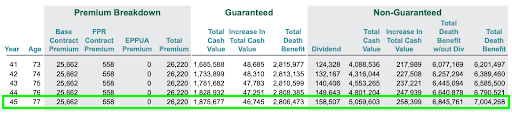

Currently, the average life expectancy in the USA is 78 years old. Let’s go further down the Illustration to look at how the Insurance Contract looks at age 77:

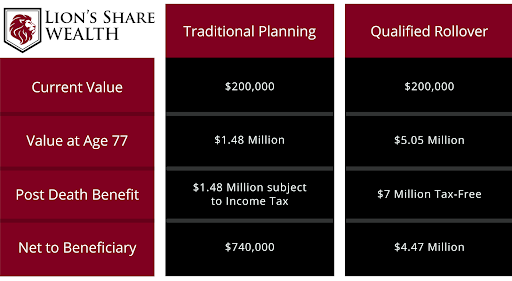

At this stage, you have a total cash value of $5.05 million, your cash value has increased by $258,000 in interest this year, and you have a total Death Benefit of $7 Million. Let’s have a look at what your legacy will look like if you were to pass away at age 77 if you have a 401(k), and if you were proactive with a Qualified Rollover:

In this comparison, I’ve taken some liberties: With a 401(k), you contribute the maximum of $20,500 per year, your employer matches 50% of your contribution (in this case $10,250 per year), the growth of a 401(k) follows market cycles and accounts for custodian fees (most financial planners omit this hard truth), and the total income rate your beneficiary pays is 50% (federal and state). With the Qualified Rollover, the growth follows the Insurance Contract rate of return only and doesn’t include gains in Crypto or other assets, and you continue to pay for the Cost of Insurance, which maintains the death benefit.

Traditional Planning is pretty straightforward: your 401(k) is worth $1.48 million when you die, your beneficiary has a tax rate of 50%, and they’re left with $740,000.

The Qualified Rollover is different; let’s break it down. Your Insurance Contract is worth $5.05 Million when you die, which is subject to a 50% tax rate, for a total of $2.52 Million left. However, we have a $7 million tax-free death benefit, automatically paying the $2.52 Million tax liability. Therefore, your beneficiary will receive a total of $4.47 million Tax-FREE. By being proactive, your heirs will be left with an additional $3.73 million compared to a 401(k). Pretty cool, right? Now, do you see why the ultra-wealthy use Life Insurance Contracts to grow their wealth from one generation to another?

At this point, you may wonder: how does the Qualified Rollover work while I’m alive?

While you’re alive, it will work exactly like a 401(k). As shown in the Venn diagram above, all your growth of investments is tax-deferred, you must take RMDs (Required Minimum Distributions) at age 72, and if you want to access your fund before you’re 59 ½ years old, there’s a 10% penalty. Note: these figures are current as of 2022 and are subject to change in the future. If you want to take distributions at age 60, the same as a 401(k), you will pay the income tax rate in the future. With a Qualified Rollover, you’re taking complete control of your destiny and hedging against future taxes and inflation with the death benefit you cannot do with your current 401(k) without penalty.

🔥Sounds complicated. Can you break it down and simplify it?

PC: I create Qualified Rollovers. They are a legal process that allows you to move your Qualified Money (401[k], IRA, 403[b], 457[b]) penalty-free and tax-free which will enable you to invest in Crypto without restriction.

🔥Take us through your daily process of what it is that you do.

PC: I wake up at 5 AM and run Robin Sharma’s 20/20/20 Formula from the book “The 5 AM Club,” which singlehandedly is the best routine I’ve ever incorporated. In short, this morning routine includes a workout for 20 minutes, meditating & journaling for 20 minutes, and reading for 20 minutes.

In terms of groundbreaking change, clarity, energy, and inner strength, nothing else I’ve done has come close to 20/20/20. I cannot recommend “The 5 AM Club” and 20/20/20 enough. Your morning dictates your day, and when you start by writing your goals for the day, you’re setting the stage for personal mastery. I can attest to doing more before noon than I used to accomplish in a week. At 7 AM, I turn my phone on to address emails & messages, and I begin making contact with past, present, and future business relationships. Every evening I journal my gratitudes and goals; I read my entry from the night before every morning. Every Friday, I evaluate my week and write my schedule for the following week to ensure it’s a success.

Success is forming a world-class team to keep your business running optimally. We all have our strengths and weaknesses, and I’ve witnessed firsthand how powerful it can be to surround yourself with people who have different strengths. No person can do everything, and you certainly don’t want to be the most intelligent person in the room.

“Surround yourself with people that know more than you.” -Henry Ford

🔥What has worked to attract and retain customers?

PC: My process of providing a Qualified Rollover is a one-time deal unless someone wants to establish another Insurance Contract down the road or has another requirement.

I do, of course, remain in contact with all clients to keep them informed of updates at Lion’s Share Wealth. Most importantly, being a resource after their Qualified Rollover and Insurance Contract is created to give an insight into how to use their new program.

I will speak to about 15 people on a given day, which encompasses past and future relationships. In-person networking groups relating to finance and investing are my preferred method to forge new relationships. In addition to in-person, I have an online presence on LinkedIn, which is an excellent way to align myself with like-minded professionals. I’m a member of several crypto-centered Telegram groups. Above and beyond in-person and online, my #1 method for attracting new business is personal referrals. It’s one thing for me to inform people of what I do, and much better to have a person I’ve worked with tell a friend or family member what I do.

Strategic Partnerships are top of my list of preferred methods to attract new business. A considerable amount of daily activity revolves around forming partnerships with experts in their field that work in unison with my offerings. I believe in synergistic relationships where a business relationship is not one-sided. So far in 2022, I’ve been a guest speaker on webinars which has been an excellent method to broaden my reach. This year, my goal is to appear as a guest on other people’s platforms, podcast episodes, and live events.

🔥Through launching Lion’s Share Wealth what is something you have learned that surprised you?

PC: Interestingly enough, high-net-worth investors are more likely to do business than most employees. Fundamentally, this comes down to a willingness to listen to new ideas. If a high-net-worth individual hasn’t heard of a strategy, they’ll listen. The same can’t be said for most employees, as some are stuck in their ways of thinking. It’s called traditional planning for a reason. Of all the rejections I’ve heard, the number #1 is that they love their CPA. I understand you probably have a strong connection with your CPA, and with a Qualified Rollover, you can keep your CPA to file your taxes if you want.

A tax professional can break down tax planning into two distinct categories: Proactive Tax Planning and Reactive Tax Planning. Proactive planning is taking steps to ensure a stable financial future and protecting your assets. Reactive tax planning is booking a time with your accountant before April 18th to find deductions. My goal is to instill proactive planning and move away from reactive planning with your tax professional moving forward.

🔥Mistakes were made. What were they and what did you do?

PC: My dba (Doing Business As) name was different from Lion’s Share Wealth when I first started. A few months into using the name, I was informed I shouldn’t use the name for compliance reasons, and I re-branded. It was a long and expensive transition to the new brand, and it was worth it in the end. I figured it was better to do it while I was relatively young and fresh instead of a year or two down the road when I’m established.

Before forming my company, I had little to no experience. It was quite the undertaking with highs and lows, and I absorbed every piece of information I came across like a sponge. I’ve had sleepless nights, the days when I felt like quitting, the days where I felt overwhelmed, and the days I questioned myself. In the end, I’m proud of what I’ve accomplished so far, and I’m thrilled about what the future holds with my endeavor.

🔥What have been the most influential things in your life that affected your project? This can include books, podcasts, or people?

PC: I’m grateful to the people who’ve been willing to assist in my learning curve and share their industry knowledge. You’d be amazed at what can happen if you ask for help. I certainly have more growing to do, and more to learn, and I look forward to sharing my accumulated knowledge with a younger generation.

Reading books is a cornerstone of my growth. My favorite books that have played a pivotal role in my life are The Monk Who Sold His Ferrari, The 5 AM Club, How to Win Through Intimidation, The Power of Zero, Becoming Your Own Banker, How to Win Friends and Influence People, Think and Grow Rich, A New Earth, and The Power of Now. The following books on my list to read are Biography of a Yogi and Tao Te Ching.

🔥Do you have any advice for other creators, entrepreneurs, or developers who want to get started or are just beginning?

PC: Spend your waking hours learning and honing your craft as your life depends on it. Learn as much as you can, and become a student of life. Never stop learning; the most prolific producers in this world don’t stop learning.

Become a student of life.

“If you want to be in the top 1% of producers, you have to be willing to do what 99% are not” -Robin Sharma

A day well scheduled is a day well spent. We all have the same amount of time in a day, and how you use it matters. Making a schedule may sound boring; however, it’s the #1 way to stay on track with your goals. Whether you know it or not, you’re already on a schedule — you may as well make it count.

Most importantly: never lose your ambition, drive, enthusiasm, or goals. Set goals so high that you cannot fail, and if you do, you’ll still love the result even if you achieve only half of what you thought. Grant Cardone is a great person to follow for goal setting and enthusiasm with his iconic 10X Rule. In essence, you 10X your goals. Instead of having a goal of $1 million in revenue, set a goal of $10 million — so if you fall short, you’re still better off than your smaller goal. I highly recommend reading his book The 10X Rule to change your professional and personal life.

🔥Where do you see the blockchain, cryptocurrency, and decentralization space going in the next 5 to 10 years?

PC: I can only answer this question from a financial perspective, as I’m not versed in code or development like many intelligent people you’ve interviewed. I’ve been saying for years that Crypto will be the future, and there are many exciting things in the pipeline. DeFi is exciting, and Blockchain is fundamentally changing the way businesses operate. Purely from a financial standpoint, cryptocurrency will be the most significant paradigm shift in our economic structure for many years to come. We’ve barely started to scratch the surface of what’s possible with this exciting new technology. It’s only been around for about 13 years now, and already it’s making a huge impact. Some countries have even started adopting Bitcoin as their national currency. In my view, we’re only getting started.

🔥Where can we go to learn more?

PC: I would be happy to speak to anyone who wants to explore a Qualified Rollover or other strategies I outlined at the beginning of this article.

Website: www.LionsShareWealth.com

Email: palmer@lionssharewealth.com

Phone: (602) 641–2911

Telegram: @PalmerLITF

Book a no-obligation free consultation: https://lionssharewealth.com/book-call.html

If you’re ready to explore a Qualified Rollover and wish to review a bespoke Insurance Contract Illustration tailored to you, please fill out this form: https://lionssharewealth.com/intake.html

Want to know how you can support Crypto Fireside?

Sign up below. It's free and easy 🔥.